Environmental Social Governance Update

EU Adopts First Set of European Sustainability Reporting Standards — Critical Considerations for Companies in Scope of CSRD

On July 31, 2023, the European Commission (Commission) adopted a Commission Delegated Act containing the first set of EU-wide European Sustainability Reporting Standards (ESRS) (Delegated Act) and accompanying Q&As supplementing the Corporate Sustainability Reporting Directive (CSRD). The CSRD, which went into effect in January 2023, extended the requirement to report on sustainability matters from a selected number of companies to all companies in the EU, except micro-enterprises.

For a summary of the CSRD’s scope and obligations, please see our Sidley Update: EU Corporate Sustainability Reporting Directive — What Do UK- and U.S.- Headquartered Companies Need to Know?

The ESRS are a set of mandatory concepts, requirements, and principles for companies to follow for non-financial reporting. Companies within the scope of the CSRD are required to report on sustainability matters (In-Scope Companies) in accordance with the ESRS. The ESRS specify the information, format, and standards for In-Scope Companies to disclose regarding sustainability matters, which cover a wide range of environmental, social, and governance (ESG) matters.

The Delegated Act (and thereby the ESRS) is expected to apply from January 1, 2024. The timing will coincide with the first phase of the application of the CSRD to EU-listed companies previously subject to the Non-Financial Reporting Directive (NFRD) and large non-EU-listed companies with more than 500 employees. These companies must publish a sustainability report in 2025, covering activities for financial years beginning on or after January 1, 2024.

Non-listed large EU companies and groups, including those whose ultimate parent is a non-EU company, must publish their first sustainability report in 2026 (for financial years starting on or after January 1, 2025). For small and medium-size companies that are listed on EU regulated markets, the first sustainability report must be published in 2027, and for non-EU parent companies affected by the CSRD’s consolidated reporting requirements (under Article 40a), the first sustainability report must be published in 2029.

This Sidley Update provides a brief overview of the newly released ESRS, as well as key considerations for In-Scope Companies to align corporate reporting policies, processes, and reporting with the ESRS.

ESRS overview

A key pillar of CSRD is its requirement for companies to undertake a “double materiality” assessment. Double materiality means assessing both (i) how a company and its value chain affect sustainability topics and other third parties (like the impact of a company on climate change); and (ii) how a company’s business could be affected by sustainability topics (like the financial risks and opportunities for a company as a result of climate change).

For any sustainability topics that are material for a company, the ESRS sets out detailed topical standards governing what a company must disclose about the material sustainability topic.

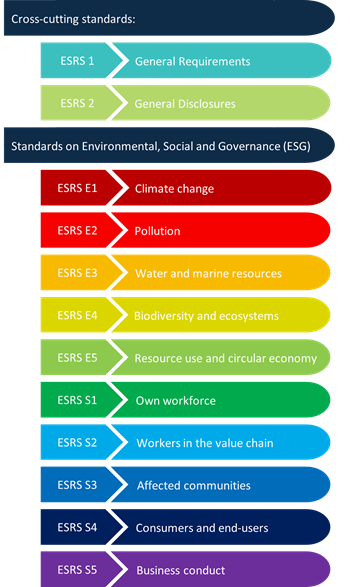

General sector-agnostic ESRS

The general sector-agnostic ESRS contain two kinds of standards:

- Two cross-cutting standards:

- ESRS 1 (General Requirements) setting out overarching reporting principles for preparing and presenting sustainability-related information (such as the double materiality perspective, time horizon, and quality of information)

- ESRS 2 (General Disclosures) setting out essential information that must be disclosed at a general level across all topical standards (such as SBM-2’s requirement to disclose how interests and views of a company’s stakeholders are taken into account by the company’s strategy and business model)

- Ten “topical” sustainability standards: The ESRS set out detailed Disclosure Requirements concerning 10 specific topical standards. There are five environmental standards, four social standards, and one governance standard, as illustrated below.

The ESRS are found in Annex 1 of the ESRS Delegated Act. Annex 2 provides definitions of the key terms.

Sector-specific ESRS and standards for small and medium-size enterprises (SMEs) and foreign parent companies

The European Financial Reporting Advisory Group (EFRAG) is preparing additional reporting standards that will be complementary or alternative to the general sector-agnostic ESRS:

- sector-specific ESRS for certain industries that will apply in addition to the sector-agnostic ESRS; the sectors for which additional standards are being developed are broad and cover quarrying and coal mining, oil and gas, road transportation, agriculture, farming and fisheries, motor vehicles, food and beverage, textiles, accessories, footwear, and jewelry

- SME-specific ESRS that will apply to in-scope SMEs instead of the full set of ESRS

- reporting standards for foreign parent companies that will apply to in-scope SMEs instead of the full set of ESRS

ESRS structure — Reporting areas

The Disclosure Requirements in ESRS 2 (General Disclosures), the “topical” (or sustainability) ESRS and, in the future, the sector-specific ESRS broadly follow a similar structure, covering the following “reporting areas”:

a) Governance: governance processes to monitor, manage, and oversee sustainability matters (e.g., ESRS 1 (General Requirements) and ESRS 2 (General Disclosures) include the requirement to provide an understanding of In-Scope Company’s due diligence process and stakeholder engagement)

b) Strategy: how the In-Scope Company’s strategy and business model interact with its material effects, risks, and opportunities (e.g., ESRS E1 (Climate Change) includes reporting on a company’s Paris-aligned transition plan for climate change mitigation)

c) Impact, risk, and opportunity management: the processes through which a company’s effects, risks, and opportunities in relation to sustainability matters are identified, assessed, and managed through policies and actions (e.g., ESRS E1 (Climate Change) includes reporting on policies related to climate change mitigation and adaptation)

d) Metrics and targets: how the In-Scope Company uses metrics and targets to track the effectiveness of its actions to manage material sustainability matters (e.g., ESRS E1 (Climate Change) includes reporting on targets set to support a company’s climate change mitigation and adaptation policies)

KEY TAKEAWAYS

ESRS applicability — Materiality assessment

In-Scope Companies should consider the following when determining which ESRS are applicable to their operations.

- Materiality assessment: As noted, In-Scope Companies must perform a double materiality assessment for all 10 ESRS topical standards. When a sustainability topic or sub-topic is material, In-Scope Companies must comply with the ESRS Disclosure Requirements for that topic or sub-topic.

If the In-Scope Company assesses the topic as not material, it can omit all Disclosure Requirements from that topical standard and may disclose a “brief explanation” for why such topical standard is not material but is not required to do so.

[Caveat regarding “detailed explanation” for conclusions for ESRS E1 (Climate Change).]

- Mandatory disclosures: Further to the above, there is also certain information that In-Scope Companies must always disclose, irrespective of the outcome of their materiality assessment:

i. the Disclosure Requirements specified in ESRS 2 (General Disclosures)

ii. in a table or indicated as “not material,” the datapoints specified in ESRS 2 Appendix B; these datapoints relate to the topical ESRS and are relevant to meet disclosure requirements under other EU legislation, for example, the principal adverse impact indicators under the EU Sustainable Finance Disclosure Regulation

iii. Disclosure Requirements (including their data points) in topical ESRS that are related to the Disclosure Requirement ESRS 2 IRO-1 (Description of the process to identify and assess material effects, risks, and opportunities) as listed in ESRS 2 Appendix C (Disclosure Application Requirements in topical ESRS that are applicable jointly with ESRS 2 (General Disclosures))

- Due diligence process: In-Scope Companies will have to report on their due diligence process. Due diligence is an ongoing process to identify, prevent, mitigate, and account for the actual and potential negative impacts connected with their operations and value chain. The engagement of stakeholders is a central part of due diligence.

The due diligence process and the double materiality assessments are closely interconnected: due diligence provides information about the effects, risks, and opportunities of the company and its value chain, which then inform the materiality assessments. As with the materiality assessments, due diligence must be adapted to account for changing circumstances over time.

- External assurance: In-Scope Companies’ sustainability reporting is subject to external limited assurance standards under the EU Accounting Directive. The CSRD currently requires limited assurance on sustainability reporting but is expected to require reasonable assurance at a later date.

- Entity-specific disclosures: If an In-Scope Company determines that an effect, risk, or opportunity is not covered (with sufficient granularity) by the ESRS but is material because of the company’s specific circumstances, it is required to make additional entity-specific disclosures regarding such effect, risk, or opportunity.

- Tailored materiality assessments: The materiality assessment may be especially demanding for certain large companies, or those with complex company structures or operations, as they will have to gather large amounts of reliable data and insights into their value chain to assess effects.

The requirement to complete a materiality assessment for each sustainability topic underlines that a one-size-fits-all approach to CSRD reports across sectors, sizes, and business models will not be sufficient under the CSRD and the ESRS. Rather, In-Scope Companies will need to tailor their sustainability policies, processes, and reporting to their particular business and its value chain in light of the ESRS. As CSRD reporting is required annually, In-Scope Companies should continuously reassess the materiality and applicability of the different ESRS.

- Aligning multiple ESG requirements: CSRD and ESRS must be considered along with compliance with other EU ESG-related due diligence and reporting requirements that may apply to a company. This includes the forthcoming Corporate Sustainability Due Diligence Directive, the Batteries Regulation, the Deforestation Regulation, and others.

Companies may also face ESG-related laws in other jurisdictions, such as the forthcoming U.S. Securities and Exchange Commission (SEC) Climate Disclosure Rule. Companies should consider these laws holistically as part of an interconnected puzzle, together with any voluntary ESG frameworks that apply (e.g., the International Sustainability Standards Board Standards (ISSB) and the Global Reporting Initiative (GRI) Standards).

- Assess applicability of the CSRD: Companies should assess whether and which entities in their corporate structure are in scope of the CSRD (and are thereby required to report in accordance with the ESRS). In addition, companies should assess when the requirements may start to apply to their corporate structure (the CSRD follows a phased implementation time frame).

- Understand the ESRS: In-Scope Companies are advised to familiarize themselves with the ESRS to prepare the internal processes necessary to assess and align reporting practice as needed before the company is due to make its first sustainability report.

- Create awareness and leadership: Reporting against the ESRS will require substantive efforts across a company, its subsidiaries, and its value chain. In-Scope Companies should initiate internal conversations across the company on corporate sustainability. In many cases, company leadership will be responsible for endorsing a strategy and steering efforts.

- Gap assessment: In-Scope companies should undertake an in-depth gap assessment to analyze their current sustainability reporting and company efforts, covering policies, processes, and company actions to determine whether CSRD/ESRS obligations are being met and, if not, where gaps exist that need to be addressed to reach full compliance.

- Conduct materiality assessments: Building on a due diligence process, In-Scope Companies should assess the materiality of each ESRS sustainability topic. In many cases, this will involve gathering a substantial amount of reliable information and data to determine whether a topic is material from a double-materiality perspective.

- Embed ESG policies and processes: Relevant sustainability and ESG reporting procedures, controls, and policies, including actions, metrics, and targets, will have to be incorporated into governance, strategy, decision-making, risk management, and accountability reporting.

- Align with reporting practices with other global standards: In-Scope companies that must comply with CSRD/ESRS must take into account other mandatory and voluntary ESG frameworks to which a company is subject (see above).

- Prepare electronic formatting: In-Scope Companies must report on the material topical standards using a standardized electronic format. This may require additional training and updates of internal processes to meet this requirement.

- Stay up to date on regulatory guidance: EFRAG also intends to periodically publish additional non-binding technical guidance on the application of the ESRS. In particular, in the near future, EFRAG expects to publish draft guidance on (i) materiality assessment; and (ii) reporting on value chains for public consultation.

Steps to align internal corporate reporting processes with ESRS

Reporting in accordance with the ESRS will require In-Scope Companies to evaluate their entire business and value chain against the topical standards set out in the ESRS.

We have summarized various considerations for this evaluation process. Note that such process will differ among companies depending on their corporate structure and level of sophistication for existing sustainability reporting processes.

律师广告—Sidley Austin LLP 是一家全球性律师事务所。我们的地址及联系方式可在 www.sidley.com/en/locations/offices 查阅。

Sidley 提供本信息仅作为向客户及其他友好人士提供的服务,且仅供教育目的使用。本信息不应被解释或依赖为法律意见,亦不构成律师与客户关系。读者在未寻求专业顾问意见之前,不应依据本信息采取任何行动。Sidley 和 Sidley Austin 指 Sidley Austin LLP 及其关联合伙实体,详见 www.sidley.com/disclaimer。

© Sidley Austin LLP

联系我们

如果您对本次 Sidley 更新有任何疑问,请联系您平时合作的 Sidley 律师,或

Offices

Capabilities

Suggested News & Insights

- Stay Up To DateSubscribe to Sidley Publications

- Follow Sidley on Social MediaSocial Media Directory