Environmental Update

Proposed Climate Disclosure Requirements for Federal Contractors Go Beyond the SEC’s Proposed Disclosures

On November 10, 2022, the federal government proposed a rule that would require government contractors to publicly disclose their greenhouse gas (GHG) emissions and set emissions reduction goals. Jointly proposed by the Department of Defense, the General Services Administration, the National Aeronautics and Space Administration, and the Office of Federal Procurement Policy in the Office of Management and Budget (OMB), the proposed rule would amend the Federal Acquisition Regulations (FAR) to require contractors to make these disclosures in order to qualify for future federal procurement contracts. Specifically:

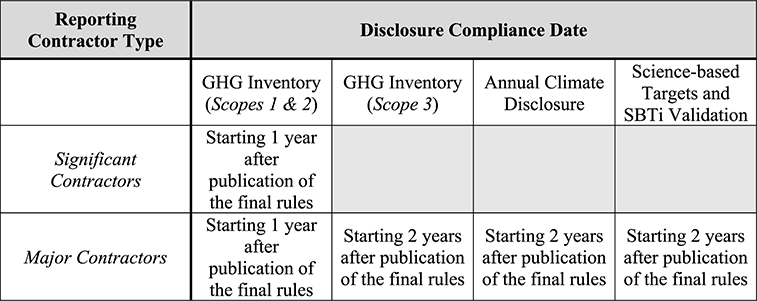

- Direct and Indirect GHG Emissions. Each “significant” contractor ($7.5 million to $50 million in annual contract obligation) and “major” contractor (above $50 million) would be required to prepare a GHG inventory of its annual direct (Scope 1) and indirect (Scope 2) GHG emissions.

- “Scope 3” Emissions. Each major contractor would also be required to disclose its Scope 3 GHG emissions. This extends beyond the contractor’s operations, to include emissions that are a consequence of the contractor’s operations, but occur elsewhere at sources other than those owned or controlled by the contractor.

- Climate Disclosure Report. Each major contractor would have to publish an annual climate disclosure report that would include a qualitative disclosure of climate-related risks.

- GHG emission reduction targets. Each major contractor would also be required to publish science-based targets to reduce GHG emissions in line with what the latest science deems necessary to meet the goals of the Paris Agreement, as validated by a third party — the Science Based Targets initiative (SBTi).

These would be expansive new requirements for government contractors — and would go even further than the extensive climate-related disclosure rules proposed by the Securities and Exchange Commission (SEC) earlier this year. Federal contractors should review carefully the implications of the proposal. Comments are due by January 13, 2023.

Background

The proposed rule is the latest action by the Biden Administration aimed at companies’ GHG emissions and the disclosure of climate-related risks. On May 20, 2021, President Biden signed Executive Order 14030: Climate-related Financial Risk and in support of that executive order later published a Roadmap to Build a Climate-Resilient Economy as part of an “all-of-government” approach to address climate change and its effects on the economy. In March 2022, the SEC issued a proposed rule that would require registrants to disclose extensive climate-related information in their registration statements and periodic reports, including disclosure of climate-related risks, the actual and potential impacts of climate-related risks, internal climate-related risk management, and reporting of direct (Scope 1) and indirect (Scope 2) GHG data, as well as additional upstream/downstream indirect GHG emissions (Scope 3) if material or if the registrant has set targets for Scope 3 GHG emissions. Parts of the SEC’s proposal rely on existing standards, such as the Greenhouse Gas Protocol Corporate Accounting and Reporting Standard (GHG Protocol) and the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD). These same standards are used in the proposed FAR revisions. However, this proposal goes further, requiring public and private federal contractors to set science-based targets and goals and quantify and report their Scope 3 emissions regardless of materiality to the contractor.

1. Categorization of Contractor Status as “Significant” or “Major” Contractor

Who is covered. The proposed rule divides federal contractors into two categories based on the dollar value of contract obligations: (i) significant contractors and (ii) major contractors that report through the System for Award Management (SAM). A “significant contractor” received $7.5 million to $50 million in total federal government contract obligations in the prior federal fiscal year, while a “major contractor” received more than $50 million in the prior fiscal year. The proposed rule would require that federal government contract obligations be calculated in accordance with OMB Circular A-11.

Exemptions. Contractors who received less than $7.5 million in total would not be subject to the rule. Also, a significant or major contractor is exempt if: (i) an Alaska Native Corporation, (ii) a Community Development Corporation, (iii) an Indian tribe, (iv) a Native Hawaiian Organization, (v) a Tribally owned concern, (vi) a higher education institution, (vii) a non-profit research entity, (viii) a state or local government, or (ix) an entity deriving 80% or more of its annual revenue from management and operating contracts that are subject to agency annual site sustainability requirements. A major contractor is also exempt from the annual disclosure and the requirement to set reduction targets if (i) a small business under the applicable North American Industry Classification System (NAICS) code or (ii) if it is a nonprofit organization but would still be required to complete and report its Scopes 1 and 2 emissions.

2. GHG Inventory

Categories of covered GHG emissions. The proposal would cover what the GHG Protocol defines as Scope 1, Scope 2, and Scope 3 emissions. Scope 1 emissions are direct GHG emissions that are owned or controlled by the reporting contractor; Scope 2 emissions are indirect GHG emissions from the generation of purchased or acquired electricity, steam, heat, or cooling that is consumed by operations owned or controlled by the reporting contractor; and Scope 3 emissions are all indirect GHG emissions not otherwise included in a reporting contractor’s Scope 2 emissions, but which occur at sources other than those owned or controlled by the entity.

Major and significant contractor reporting. One year after a final rule, both significant and major contractors would be required to have completed a GHG inventory of both Scope 1 and Scope 2 emissions based on the requirements of the GHG Protocol. Reporting contractors would be permitted to use the emissions calculation tool of their choice, as long as it aligns with the GHG Protocol, and must represent emissions during a continuous period of 12 months, ending not more than 12 months before the inventory is completed.

Scope 3 Emissions. Two years after any final rule, major contractors would also be required to conduct a GHG inventory for their Scope 3 emissions, which likewise would have to be calculated based on GHG Protocol requirements and reflect emissions during a continuous period of 12 months, ending not more than 12 months before the inventory is completed.

3. Annual Climate Disclosure

Two years after a final rule, a major contractor would need to complete an “annual climate disclosure.” This disclosure would align with the TCFD. The TCFD covers governance, strategy, and risk management, as well as metrics and targets across two major categories: (i) risks related to the transition to a lower-carbon economy, and (ii) risks related to the physical impacts of climate change. It would be prepared based on the elements of the CDP Climate Change Questionnaire that align with the TCFD. CDP is an international non-profit that runs a global environmental disclosure system that provides a standardized format for GHG emissions and climate change disclosures. The annual climate disclosure would have to be made available on a publicly accessible website.

4. Science-based Targets and SBTi Validation

Beginning two years after a final rule, major contractors would have to develop science-based climate targets and have such targets validated by a third-party, the SBTi. SBTi is a partnership among CDP, the United Nations Global Compact, the World Resources Institute, and the World Wide Fund for Nature, whose stated goal is to provide a pathway for companies to reduce GHG emissions to meet the goals of the Paris Agreement. Major contractors would commit to set a science-based target, which would be posted on the SBTi website. Once a contractor makes a commitment, it would have 24 months to submit its targets, which would likewise be published after receiving SBTi validation. Following validation, reporting contractors would monitor progress toward reaching its targets, which SBTi must revalidate at least every five years.

5. Responsibility Determination

Compliance is necessary for contractor to be deemed “responsible.” Importantly, the proposal would make these new requirements as a basic precondition for a significant or major contractor to contract with the government. Under the FAR (FAR 9.1.03(a)-(b)), federal contracts or purchases are awarded only to “responsible” contractors. Under the proposed rule, a significant or major contractor would be deemed “nonresponsible” and thus would not qualify for an award, unless the contractor complies with these new requirements.

Exemption, Waiver and Extensions. The proposal does outline procedures through which a contractor could receive an exemption, a waiver, or additional time to comply. For example, a contractor exempt from the requirement to be registered in the SAM would be exempt under the proposal. Further, a contractor may receive a waiver for national security purposes, or for emergencies, national security, or other mission-essential purposes. A contractor that does not comply may still be responsible if (i) the noncompliance resulted from circumstances beyond the contractor’s control, (ii) the contractor provided documentation that demonstrates substantial efforts to comply, or (iii) the contractor has made a public commitment to comply within one calendar year. Along the same lines, a contracting officer may also provide a contractor an additional year to come into compliance with the proposed rules.

Proposed Compliance Dates

The proposed phase-ins for the compliance dates of the proposed rule.

Next Steps for Reporting Contractors

Although the rule is not yet finalized, there are practical steps for contractors to take:

- Evaluate how the proposed rule would impact your operations. Reporting contractors should begin assessing the gaps between climate-related information they currently disclose or otherwise collect and what would be required under the proposed rule, if adopted. These gaps could be significant for many contractors that previously have not had to disclose such information. Even contractors that have complied partially with TCFD disclosures may need to rework their approach or expand their disclosures to satisfy the proposal.

- Evaluate the impact of noncompliance. Noncompliance with these proposed disclosure requirements could mean that a contractor would be deemed nonresponsible and lose out on any future government purchases or contract awards. Contractors should assess how quickly they could gather the required information to comply with the proposal if implemented.

- Evaluate how the proposed rule would impact your operations. If adopted, the rule may impact operations, as reporting contractors may be compelled to take actions to adjust monitoring, accounting, planning, and governance practices, as well the processes, personnel, policies, and technologies that would be needed to meet science-based targets.

- Identify the disclosure obligations that would be challenging for your enterprise to meet. Many of the proposed disclosure requirements would create new challenges for reporting contractors that have not made these disclosures in the past, such as the disclosures of Scopes 1 and 2 — and especially Scope 3 emissions.

- Participate in the comment period. The government must consider and respond to public feedback when drafting final rules. Hence, stakeholders impacted by the proposal should consider providing input on the proposed rules. Comments are due by January 13, 2023.

For additional information on the topics covered in this update and current issues around climate-related rulemaking and other federal agencies, see recent publications of Sidley Austin LLP on our practice pages for Public Companies, ESG, Capital Markets, and Corporate Governance and Executive Compensation.

弁護士広告—Sidley Austin LLP はグローバルな法律事務所です。当事務所の所在地および連絡先情報は、www.sidley.com/en/locations/offices に掲載されています。

Sidley は、本情報をクライアントおよび関係者の皆様へのサービスとして、教育目的のみに提供しています。本情報は、法的助言として解釈または依拠されるべきものではなく、また弁護士と依頼者の関係を生じさせるものでもありません。読者は、専門家の助言を求めることなく本情報に基づいて行動すべきではありません。Sidley および Sidley Austin とは、www.sidley.com/disclaimer に記載のとおり、Sidley Austin LLP およびその関連パートナーシップを指します。

© Sidley Austin LLP

お問い合わせ

この Sidley Update に関してご質問がある場合は、通常ご担当されている Sidley の弁護士、またはご連絡ください。

Offices

ません Related Resources ません

関連公式ブログ

得意分野

Suggested News & Insights

- Stay Up To DateSubscribe to Sidley Publications

- Follow Sidley on Social MediaSocial Media Directory