Tax Update

One Step Forward: Ways and Means Committee Approves Expanded Renewable Energy Tax Credits

On September 15, 2021, the House Ways and Means Committee approved the tax provisions in the Build Back Better Act (the Bill) as part of the budget reconciliation legislation process.

As described more fully below, the Bill includes several provisions relating to renewable energy, including provisions

(i) expanding and extending existing tax credits provided by Section 451 (the production tax credit (PTC)), Section 48 (the investment tax credit (ITC)), and Section 45Q (the Carbon Capture Credit), including the extension of the ITC to standalone energy storage projects

(ii) creating a tiered tax credit system that encourages compliance with prevailing wage and apprenticeship requirements and use of domestically produced materials

(iii) introducing a “direct pay” option

(iv) creating new tax credits for various technologies

(v) modifying the rules applicable to “publicly traded partnerships” in a manner that would facilitate investments in renewable energy by those partnerships

Key Takeaways

Although subject to continuing debate and negotiation in Congress, if enacted, the Bill is expected to significantly boost investments in renewable energy projects and advance the Biden administration’s goals to reach net-zero emission by 2050 and generate 80% of the nation’s electricity from clean energy sources by 2030.

The proposed expansion and extension of the PTC, the ITC, and the Carbon Capture Credit (as well as the new ITC for standalone energy storage projects) should support the ongoing growth of the various renewable energy technologies and lead to new installations and financing of new projects for years to come.

In addition, providing new tax credits for various technologies that are currently not benefiting from similar incentives should contribute to the continued development and growth of such technologies.

The direct pay option as well as the changes to the publicly traded partnership rules could expand the pool of investors in renewable energy and allow for certain projects, which otherwise would have had encountered financing difficulties, to be completed.

As further discussed below, to incentivize higher worker pay and job creation, the Bill introduces a two-tiered credit system, with a “base rate” and a “bonus rate,” depending on whether the project meets specific wage and apprenticeship requirements. To qualify for the full tax credits, the project would need to meet these new requirements. If enacted, it remains to be seen what effect the prevailing wages and apprenticeship requirements (as well as the domestically produced materials provisions) would have on the cost of the development and construction of the projects, the needed compliance processes, deals’ structure, and the risk allocation among the various industry participants.

PTC and ITC Extension and Expansion

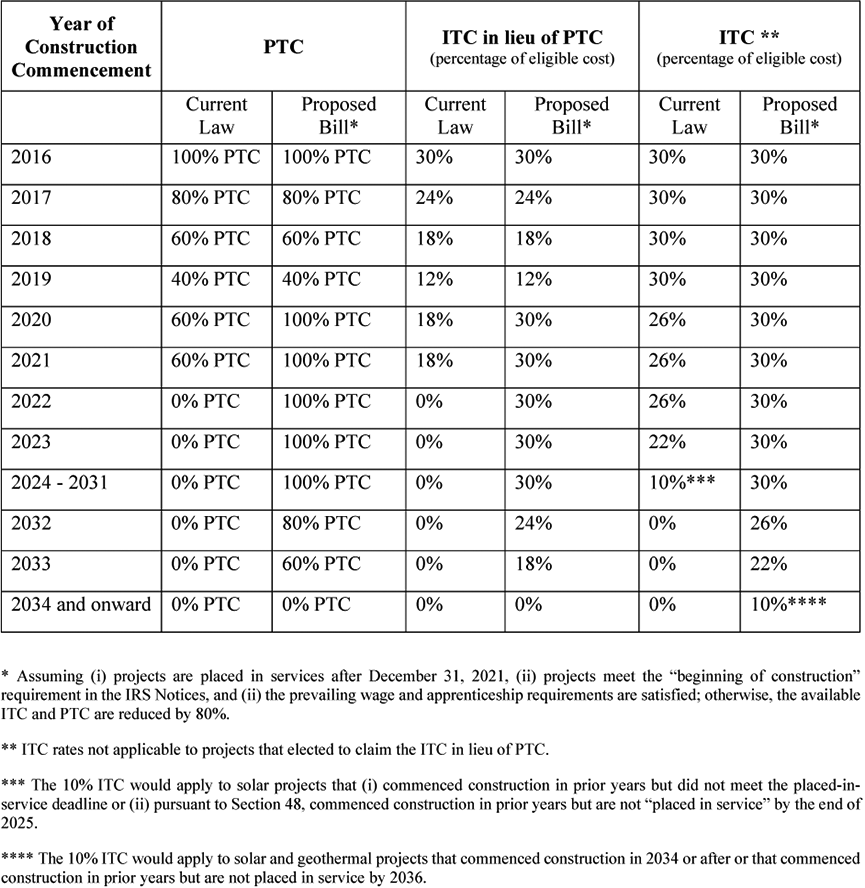

The PTC. The PTC is currently available for the 10-year period beginning on the date the project is placed in service and is equal to a specified amount (currently 2.5 cents) per kilowatt-hour of electricity generated by the project and sold to an unrelated person.

The PTC for wind projects is currently subject to a phasedown schedule that applies to wind projects commencing construction after 2016.

The Bill makes a number of changes to the PTC.

First, projects beginning construction after 2019 and before 2032 will be eligible for the full inflation-adjusted PTC. These projects include projects beginning construction in 2020 or 2021 that are eligible for only 60% of the full PTC under current law but only to the extent those projects are placed in service after 2021.

Accordingly, the Bill would increase the PTC available for projects beginning construction after 2019 that are placed in service after 2021 (from 60% of the full PTC to 100% of the full PTC). Taxpayers with projects that began construction in 2020 or 2021 should continue to monitor this legislation, as it may be beneficial to delay the “placed in service” date for those projects to a post-2021 date.2

A new phasedown schedule would apply to projects beginning construction after 2031. The PTC would be reduced to 80% of the full PTC for projects beginning construction in 2032, 60% for projects beginning construction in 2033, and zero for projects beginning construction in 2034 and onward.

Second, the Bill would reinstate a rule that has expired, allowing owners of solar projects to elect to receive the PTC.

Third, the Bill would implement a two-tier credit system to projects beginning construction after the Bill is enacted, subject to an exception for small (less than 1 MW) projects. To qualify for the full PTC, projects will need to meet new prevailing wage and apprenticeship requirements. These requirements are discussed more fully below. Projects failing to meet these requirements would be eligible only for the “base” rate of 20% of the otherwise applicable PTC amount.

Finally, as discussed more fully below, the Bill would increase the PTC amount otherwise applicable to projects satisfying certain “domestic content” requirements.

The ITC. The ITC is claimed as a percentage of the project’s eligible cost, up to 30%. Projects that began construction before 2020 are currently eligible for the full 30% ITC, while certain projects beginning construction after 2019 are subject to a phasedown schedule.

The Bill would make several changes to the ITC similar to the changes made to the PTC.

First, projects beginning construction prior to 2032 would be eligible for the full 30% ITC. These projects would include solar, geothermal, or fuel cell projects beginning construction in 2020 or 2021 that are eligible for only the 26% ITC under current law but only to the extent those projects are placed in service after 2021.

The 30% ITC would phase down to 26% for projects that begin construction in 2032, to 22% for projects that begin construction in 2033, and to 10% for solar and geothermal projects beginning construction in 2034 or later or that are not placed in service by January 1, 2036. No credit is allowed with respect to eligible property, other than solar and geothermal projects, if such property commences construction after 2033 or is not placed in service before 2036.

Second, as with the PTC, a two-tier system would be adopted for projects beginning construction after the Bill’s enactment, subject to an exception for small (less than 1 MW) projects. To qualify for the full ITC rates, projects would need to meet new prevailing wage and apprenticeship requirements described more fully below. Projects failing to meet these requirements would be eligible for the base ITC rate equal to 20% of the otherwise applicable ITC rate.

Finally, as with the PTC, the otherwise applicable ITC rate would be increased for projects satisfying the “domestic content” requirements described below.

ITC for Standalone Storage

The Bill includes a long-awaited ITC for standalone energy technology. Energy storage technology includes equipment that uses batteries, compressed air, pumped hydropower, hydrogen storage, and certain other storage property used to store energy for conversion to electricity (or, in the case of hydrogen storage, to store energy) with a capacity of at least 5 kWh. These properties would be subject to the same phaseout schedule applicable to the non-solar, nongeothermal energy property.

Enacting this new ITC for standalone storage facility is a significant change to the current rules governing energy storage property, which allow an ITC to be claimed only if the storage equipment is part of an otherwise ITC-eligible project and certain other requirements are met.

Extensions of Election to Claim the ITC in Lieu of the PTC

Under current law, owners of certain facilities otherwise eligible for the PTC can elect to receive the ITC in lieu of the PTC. The Bill would extend the availability of that election for projects beginning construction prior to 2033.

The table below summarizes certain of the described changes to the PTC and ITC provisions.

Section 45Q Tax Credit for Carbon Oxide Sequestration

Under current law, taxpayers who use carbon capture equipment to capture qualified carbon oxide from an industrial facility or from the atmosphere and sequester it, or use it for certain purposes as provided by Section 45Q, are eligible for the Carbon Capture Credit for each metric ton of qualified carbon oxide captured (the amount of which currently ranges from $10 to $50 per metric ton) over a 12-year period starting on the date the equipment is first placed in service.

The Bill would expand the Carbon Capture Credits for qualified facilities that begin construction before January 1, 2032, and eliminate the liner interpolation of the credits by replacing it with an immediate increase of the credit amount to $50 per metric ton of carbon oxide captured and sequestrated, for otherwise qualified projects, and to $35 per metric ton of carbon oxide captured and used as a tertiary injectant or for an otherwise approved purpose.

For “direct air capture facilities,” the Bill would increase the applicable credit amount to $180 per metric ton of carbon oxide captured and sequestered and to $130 per metric ton of carbon oxide captured and used as a tertiary injectant in a qualified enhanced oil or natural gas recovery project or otherwise used in an approved manner.

The Carbon Capture Credits would also be subject to the prevailing wage and apprenticeship requirements and to the lower “base” rate if such requirements are not met.

Finally, although the Bill reduces the minimum threshold amount of carbon oxide required to captured in order to receive the credit, it includes a new requirement for a recapture of a minimum of 75% of the carbon oxide that would otherwise be released by the electricity-generating facility (or 50% in the case of other emitting facilities). This new requirement could prove to be a challenge for some developers and facilities.

Many developers have asked for an increase of the general credit amounts from the current $50 (or $35) per metric ton based on their view that the current credit amounts are not sufficient to allow for the efficient development and financing of such projects. The Bill does not address this request.

Prevailing Wage and Apprenticeship Requirements

For qualified projects to be eligible to claim the credits at the full (“bonus”) rate, the taxpayer must ensure that any laborers and mechanics employed by contractors and subcontractors are paid prevailing wages during the construction of such project and, in some cases, a defined period after. Projects failing to meet these requirements would be eligible only for the “base” rate of 20% of the otherwise applicable credit amount.

In the event the taxpayer fails to satisfy these requirements, the taxpayer may cure the failure by paying each worker the difference between actual wages paid and the prevailing wage, plus interest, in addition to paying a $5,000 penalty for each worker paid below the prevailing wage during the taxable year.

In addition, to claim the “bonus” rate, taxpayers also must ensure that no fewer than the applicable percentage of total labor hours are performed by qualified apprentices. The applicable percentage is 5% for projects for which construction begins in 2022, 10% for projects beginning construction in 2023, and 15% thereafter. Each contractor and subcontractor who employs four or more individuals to perform construction on an applicable project shall employ at least one qualified apprentice.

In the event of a lack of available qualified apprentices necessary to satisfy this requirement, taxpayers can show a good faith effort was made to hire qualified apprentices to be exempt from this requirement.3

These new requirements are likely to create some commercial concerns and would affect the economics of these projects by increasing their construction cost as well potentially affecting the financing opportunities due to the relative uncertainty that the projects could meet such requirements. As such, if enacted, these requirements will require careful planning and negotiations, especially with the EPC and O&M contractors as relates to risk allocation and compliance issues.

Domestic Content Requirement

Projects could be eligible for a 2% increase to the “base” tax credit rate (for projects of 1 MW or greater not satisfying the wage and apprenticeship requirements) or a 10% increase to the “bonus” rate (for projects with a maximum net output of less than 1 MW and other projects satisfying those requirements) if they meet the domestic content requirement.4 To qualify for this additional credit, taxpayers must ensure that the steel, iron, or other manufactured products that comprise the project were produced in the United States. A product will be considered manufactured in the United States if not less than 55% of the total cost of the components of such product is attributable to components that are mined, produced, or manufactured in the United States.

The Direct Pay Election

The Bill includes a new direct pay option, which in essence converts the applicable tax credit to a refundable credit, for projects that are placed in service after December 31, 2021. Taxpayers that make this election would be treated as having made a tax payment equal to the value of the applicable tax credits they would otherwise be eligible to claim and could then claim a refund for the excess taxes they paid or deem to have paid.

Projects that satisfy the domestic content requirement (or have a maximum net output of less than 1 MW) would be eligible for a direct pay equal to 100% of the applicable tax credit amount. Starting in 2024, projects not satisfying the domestic content requirement would be subject to a phasedown of the applicable percentage available for the direct pay election. Such projects would be subject to a 10% reduction (and therefore eligible only for a 90% direct pay) if they commence construction in 2024, 15% reduction if they commence construction in 2025, and 100% reduction (and no direct pay available) if they commence construction in 2026 or thereafter.

This election would be available for a number of green energy credits, such as the PTC, ITC, Carbon Capture Credits, and the new transmission property credit and the clean hydrogen credit.

Rules similar to the ITC recapture rules and basis adjustment rules of Section 50(c) would apply for purposes of the direct-pay provisions.

Although some of these tax credits could be subject to a reduction if the project is owned, directly or indirectly, by tax-exempt entities, the direct-pay option will nevertheless be available, without any such reduction, even if such tax-exempt ownership exists. Allowing tax-exempt entities to directly or indirectly own these projects and still be eligible for the full direct pay would potentially expand the pool of investors in such projects to include pension funds, investment funds, and other tax-exempt investors.

The direct-pay option would provide developers that otherwise have difficulties financing their projects using the traditional tax equity financing to forgo such financing and claim the direct pay instead. Debt financing may be needed, at times, to bridge the timing gap between when the project is placed in service and when the tax refund for that year is received. This alternative would be a welcome development to many developers; however, it is not expected to eliminate the need for some tax equity financing, either to allow for the monetization of the accelerated depreciation available for such facilities, for projects subject to the phasedown of the direct pay amounts or for other commercial or financial reasons.

New Credits

PTC for Clean Hydrogen Credit. The Bill adds Section 45X providing for a new PTC for the production of clean hydrogen at a qualified facility during the 10-year period following the facility placed-in-service date. The credit would be available for projects that commenced construction after 2021 and before 2029.

The annual credit amount would equal the number of kilograms of qualified clean hydrogen produced by the taxpayer multiplied by $3 multiplied by an applicable rate. The applicable rate is 20%, 25%, 34%, or 100% depending on the reduction percentage of the lifecycle greenhouse gas emission.

The Section 45X credit would be subject to prevailing wage and apprenticeship requirements.

No credit will be available for a facility that could claim the Carbon Capture Credit. However, the Bill allows projects to receive both the PTC for electricity produced from renewable resources and the Section 45X clean hydrogen credit. Taxpayers could also claim ITC in lieu of the Section 45X PTC.

ITC for electric transmission property. The Bill adds Section 48D providing for a tax credit equal to 30% of the basis of qualifying electric transmission property, the construction of which commences after 2021 and that is placed in service before 2032.

The Section 48D credit is subject to the same prevailing wage and apprenticeship requirements as the ITC and is eligible for the 10% increase for projects meeting the domestic content requirement.

Qualifying electric transmission property is defined as tangible, depreciable property that is an electric transmission line that is capable of transmitting electricity at a voltage of not less than 275 kilowatts and has a transmission capacity of not less than 500 megawatts as well as other transmission property owned by the same taxpayer. No credit is allowable with respect to related transmission property unless the taxpayer is also allowed a credit for the qualifying electric transmission property to which it relates.

Zero emissions facility credit. The Bill adds Section 48E, which would provide a credit equal to 30% of the basis of any zero-emissions facility placed in service by the taxpayer. A zero-emissions facility is any facility that generates electricity, does not generate any greenhouse gases, and uses a technology or a process that produces less than 3% of the overall electricity production in the United States. The zero-emissions facility credit would be subject to an overall annual limitation of $250 million for each of the calendar years 2022 through 2031, and the credit expires thereafter.

Other Credits. The Bill also includes credits for other technologies, such as an increased ITC for solar facilities with a nameplate of 5 MW or less in low-income communities; the Section 45W credit for electricity produced at a qualified nuclear power facility; the Section 40B sustainable aviation fuel credit with respect to sales and uses of a qualified fuel mixture; and specific tax credits for the purchase of a used plug-in electric car and qualified commercial electric vehicles.

Green Energy and Publicly Traded Partnerships

“Publicly traded partnerships” are currently subject to taxation as corporations unless at least 90% of their gross income consists of “qualifying income.” Qualifying income includes passive income and income and gains from various oil- and gas-related operations.

The Bill would expand these rules governing “publicly traded partnerships” to include other types of income and gains, such as income from the generation of electric power or thermal energy from qualified energy resources under Section 45 and Section 48, open-loop biomass, or municipal solid waste and from the operation of a carbon capture facility.

The inclusion of renewable energy projects in the category of assets that produces good qualifying income for purpose of testing the “publicly traded partnership” could increase the pool of potential investors and provide additional, relatively inexpensive forms of financing for developers of renewable energy projects.

1Unless otherwise specified, all references to “Section” are to the Internal Revenue Code of 1986, as amended (the Code).

2The phaseout percentages currently in effect will continue to apply to projects that (i) began construction prior to 2020 regardless of when they are placed in service and (ii) projects that began construction in 2020 or 2021 that are placed in service before January 1, 2022.

3The summary of the Bill prepared by the House Ways and Means Committee also contains a cure provision for the failure to meet the apprenticeship requirement, according to which a taxpayer may cure the discrepancy by paying a penalty equal to $500 multiplied by the total labor hours for which the requirement is not satisfied. This provision, however, is not included in the legislative text of the Bill.

4Thus, (i) in the case of a wind facility that would otherwise qualify for the PTC at the “bonus” rate of 2.5 cents per kw/h, the PTC rate would increase to 2.75 cents per kw/h and (ii) in the case of a solar facility that would otherwise qualify for the ITC at the “bonus” rate equal to 30%, the ITC rate would be increased to 40%.

Attorney Advertising—Sidley Austin LLP is a global law firm. Our addresses and contact information can be found at www.sidley.com/en/locations/offices.

Sidley provides this information as a service to clients and other friends for educational purposes only. It should not be construed or relied on as legal advice or to create a lawyer-client relationship. Readers should not act upon this information without seeking advice from professional advisers. Sidley and Sidley Austin refer to Sidley Austin LLP and affiliated partnerships as explained at www.sidley.com/disclaimer.

© Sidley Austin LLP

Contacts

If you have any questions regarding this Sidley Update, please contact the Sidley lawyer with whom you usually work, or

Related Resources

Capabilities

Suggested News & Insights

- Stay Up To DateSubscribe to Sidley Publications

- Follow Sidley on Social MediaSocial Media Directory